LVMH and The Luxury Strategy

A deep dive into luxury brand management

I recently read The Luxury Strategy by Jean-Noël Kapferer, the book that is considered the definitive guide to understanding luxury consumer brands. The principles examined in it were really insightful, and while I originally intended to post up some book notes on it, what I thought would be more interesting was to discuss some of these ideas through the lens of their application to a company that’s been a core holding of mine, the French luxury giant Moet Hennessy - Louis Vuitton (LVMH). After reading this book and understanding the complexity and expertise required to manage luxury brands successfully, my appreciation for the strengths of LVMH has significantly deepened.

As a quick intro to LVMH, the company was established in 1987 through the merger of Louis Vuitton (a French leather goods and fashion house) and Moet Hennessy (a wine & spirits producer). In 1988 with the help of Diageo (then Guinness) enterpreneur Bernard Arnault took a 24% stake in LVMH, and through a series of shrewd moves, maneuvered his way to becoming CEO the following year. By 1994 the Arnault family was the controlling shareholder as Diageo sold down their stake, and as of 2021 they owned 47.8% of LVMH shares and 63.5% of the voting rights. Bernard, currently 73, is still CEO and Chairman, and his children (below) all have various senior roles across the company. Despite being a public company, LVMH is very much a family-run business. This gives them the latitude to think inter-generationally and invest for the long-term, which is crucial for luxury brands.

Under the helm of Arnault, LVMH has been consolidating the luxury industry and has become the largest luxury conglomerate in the world. It currently has 75 Maisons (or Houses) of some of the world’s most recognised brands across leather goods, fashion, jewelry, alcohol, perfumes.

The Fashion and Leather Goods segment is the largest segment, accounting for c. 50% of group revenue and c. 70% of group EBIT. Within this segment, the iconic Louis Vuitton is by far the most important brand, estimated to account for c.60% of its revenue and 70% of its EBIT, making it the single largest contributor to the overall group. The second most important brand is Dior, which is growing much faster than Louis Vuitton and the overall Fashion and Leather Goods segment. LVMH owns a stable of other brands across its segments: Fashion & Leather Goods - e.g. Fendi, Celine, Kenzo; Wine & Spirits - e.g. Moet & Chandon, Dom Perignon, Hennessy; Watches and Jewelry - e.g. Bulgari, TAG Heuer, and Tiffany most recently; as well as retailers Sephora and DFS. A list of their assets is shown in the chart below. Given the disproportionate importance of Louis Vuitton and Dior however, these two brands will be the primary focus of this article, although towards the end I will briefly touch upon how the luxury playbook is being applied to LVMH’s brands in other segments as well.

The essence of luxury

“The more you see a behavior throughout history, the more you realize how ingrained it is in human behavior, which makes you more confident that it’ll be part of our future”

Morgan Housel - Engaging with History

Since the dawn of man, humans have had a deeply innate desire to status-seek, differentiate and elevate themselves from others. Hunter gatherers buried their dead with precious ornaments and symbols of power, Egyptians built extravagant pyramids for their pharaohs, and in the centuries that followed class systems were deeply embedded in the social fabric of just about every culture, which meant vastly different living standards between the rich and poor. Since the 19th century’s Industrial Revolution however, the world has been becoming increasingly democratized and meritocratic, and as such class systems have become much less prevalent. So to elevate themselves, people have increasingly turned to other means.

Even though the Arnault family refutes this point publicly, undoubtedly luxury brands have become a legitimized means of creating that social stratification and status signaling. As long as it serves this innate human desire, the luxury industry will continue to have a permanent place in the world. In the book Kapferer reminds us that it is by spending on non-productive items that people signal their rank.

“Here lies the difference between luxury and premium. People buying premium or even super-premium like to justify every dollar by a return on investment. Premium means pay more, get more in functional benefits. Luxury is elsewhere: it signals the capacity of the buyer to transcend needs, functions, or objective benefits”

The Luxury Strategy

The ability for luxury to serve this important social function comes from creating desire around the brand - making people dream for it. Bernard himself continuously expresses that ‘creating desire’ is the most important part of what they are doing at LVMH. This is a challenging task, because managing a luxury brand requires balancing competing tensions:

The tension between scarcity (restricting access, creating desire) and diffusion (growth and sales).

The tension between timelessness/heritage, and modernity/innovation

The laws of managing and marketing luxury brands are very different and in some cases opposite to that of traditional consumer products. The Luxury Strategy is famous for its Anti-Laws of Marketing for luxury brands, which I have included here as an attachment. I will refer to these throughout the article.

Scarcity vs. growth - maintaining desirability at scale

“For luxury brands, the perceived diffusion kills the dream through the loss of exclusivity and therefore the loss of the social driver of luxury, and of the impulsion of the desire of others. It is therefore necessary to reduce diffusion, and increase the obstacles to accessing the brand.”

The Luxury Strategy

Luxury is one of the only sectors where growth creates a problem as it can lead to loss of cachet and desirability. The challenge for companies like LVMH is to grow desirability faster than diffusion. Scarcity needs to be created, which is done through both physical scarcity (premium pricing, restrictions to access), or virtual scarcity (through other psychological means such as marketing).

Pricing strategy

Probably by far the most important element of establishing exclusivity is premium pricing - making the products out of reach of majority of the people. However, this only works if a brand has strong desirability and brand equity. The stronger one desires for something, the less relevant price becomes, allowing you to 'name your price', in contrast to a commodity, where the producer is a price-taker. Brands that can maintain high visibility and therefore high value perception over time have a license to print money, and this can earn them returns on invested capital far above those seen in other industries. This relationship between brand equity/desirability and pricing power is at the very heart of luxury brand management. Jean-Jacques, CFO of LVMH, addressed this point directly during the Q3 earnings call:

Second question on basically on pricing power. I mean, every time -- this question is always structured the same way. I mean, it seems like pricing power is a sort of windfall -- comes from the sky. And some brands have it and some brands have not. The reality is that pricing power is actually a function of the desirability of the brand. Desirable brands can increase prices and non-desirable brands cannot. It's as simple as that. So what it is about is really developing strategies, marketing, products, distribution strategies that will increase desirability of the brand, so that in tough times or in other times, we can reflect into prices the cost of doing business. It's as simple as that.

So when you look at Vuitton and Dior, that's what they've done, by and large. And therefore, they enjoy a significant pricing power…It did not happen overnight. It's something that has been created patiently over years and years and years so that the desirability of the brand is such that clients accept it.

Jean Jacques Guiony (CFO), Q3’22 earnings call

I will touch upon various aspects of building brand equity later in the piece. Assuming however that brand equity and desirability exists, Kapferer suggests two pricing rules that luxury brand should abide by:

Raise your prices as time goes on in order to increase demand (Anti-Law #13)

Keep raising the average price of the product range (Anti-Law #14)

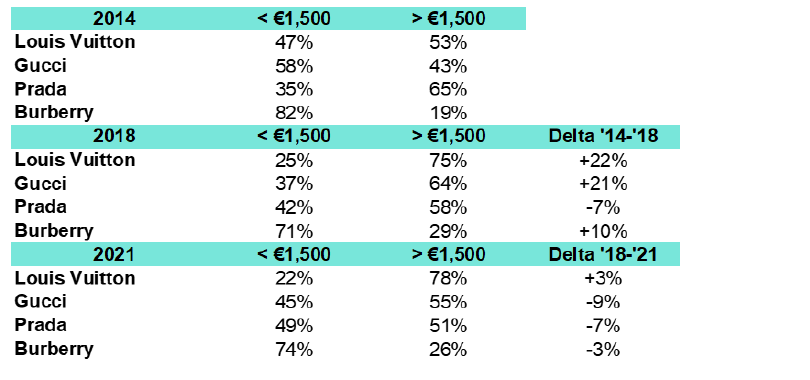

Louis Vuitton, Dior, and a handful of its pure luxury competitors including Hermès and Chanel have perfect price discipline and distribution grip — they sell 100% retail and 100% at full price. This allows them to follow a strict policy of putting through annual price increases well above inflation. This is best seen in following the price of a specific product. For example, we can see below that over a 40 year time period Louis Vuitton’s Speedy 30 handbag’s price has grown at a CAGR of 5%. Dior has also been consistently raising its prices as it establishes itself as a high-end luxury brand, as shown below for its iconic Lady Dior handbag.

On the point of the upward progression of the average selling price, we can see below how effective Louis Vuitton has been in moving its assortment to higher price ranges through introduction of higher priced product lines.

Of course that doesn’t mean that a luxury brand can’t introduce lower priced products as a of way of initiating customers into the brand universe - like Louis Vuitton does with small leather goods (wallets and purses etc). However, what is crucial is that if you’re going to introduce products in the lower price range, you also need to increase the number of products at the upper end of the range, in order to maintain the overall average price and not dilute the brand’s status. This is exactly what Dior has done. For example in the beauty range, it generally has more products than its competitors in the lower priced categories, but also has the widest price range with the maximum price point stretching far higher than its peers (the yellow circles in the chart below, based on TMall data in China from Bernstein).

Louis Vuitton and Dior, as pure luxury brands focusing on leather goods, abide by strict pricing rules, and it’s a bit easier to do this when you are dealing with leather goods which are non-perishable and not subject to seasonality. Other brands (including some owned by LVMH) that are less pure luxury and more ready-to-wear fashion are not necessarily as disciplined (e.g. Gucci, Kenzo, Burberry, Prada, Ferragamo, etc.) and are using their outlet networks to clear inventory - a better solution than lowering prices in the store.

I will come back to what pricing power means for profitability a bit later.

Product quality

In a world where information flows freely and consumers are becoming better researched and discerning, in order to justify premium prices it becomes even more important for luxury brands to ensure that the products are of the highest quality possible. Under Arnault, LVMH pioneered the playbook of vertical integration and having very strict control over the entire product supply chain, from sourcing of materials to production to retail. This ensures that products are of the highest quality and standard, and sales are tightly controlled through own store networks (a key source of physical scarcity). LVMH has purchased tanneries other material suppliers across Europe, trains its own artisans in vocational programs through its University of LVMH, and has many of its key products made by hand. Each Louis Vuitton trunk can take up to 60 hours to make, while a suitcase can take up to 15 hours.

Unlike commodity products, most of the production normally takes place in high cost countries, usually the country of the brand’s origin. This point is key - Kapferer says the moment a luxury brand offshores the production of its central product, it risks impairing its luxury status (Anti-Law #18: Don’t relocate your factories):

“When someone buys a luxury item, they are buying a product steeped in a culture or in a country. Having local roots increases the perceived value of the luxury item”

The Luxury Strategy

Not only does moving production offshore result in risk of lower quality, but the brand’s image is often tied to its birth place and is a source of differentiation in a world that is increasingly globalised. This is why Louis Vuitton produces primarily in France, although select products are produced in facilities in Spain, United States, Germany and Switzerland with imported materials (only hand chosen materials are used).

Distribution and inventory management

“Distribution is generally the weak link of luxury strategy, and this is where many brands die”

The Luxury Strategy

Hand in hand with pricing, inventory management and distribution is critical to ensuring physical scarcity (Anti-Law #5: Don’t respond to rising demand; Anti-Law #7: Make it difficult for clients to buy).

As it relates to inventory, most of the luxury brands limit the volume of production. As described by Louis Vuitton’s CEO Michael Burke in 2018 - “LV plans tension in its inventory on purpose, always making one too few “. Generally not the entire range will be available in store, meaning a waiting period is required, although this is typically much shorter than than those for Hermes’ Birkin bag (2 years) and Kelly bag (6 months). By making consumers “work” to receive the product, desire is increased. Famously, Louis Vuitton would also rather incinerate unsold items than discount them, all for the purpose of maintaining long-term brand equity rather than maximising short-term profits.

Controlled distribution is also of paramount importance. Louis Vuitton was one of the first to implement an own store network and strictly no wholesale. Louis Vuitton stores are always in prime locations, and many are architecturally designed, almost like galleries, making a bold statement that is visible to all. The fixed costs of setting up and running own brand stores like this are extremely high, which is why only mega-brands can afford to do this, creating a barrier to entry for smaller brands. In turn however, the gross margins are much higher due to elimination of intermediaries. Kapferer makes this point clear specifically in relation to Louis Vuitton’s competitive advantage:

“The [own store network] system is very effective: we calculated at the time that a competitor, not having integrated its production and not selling through its own network, would have had to sell a bag at twice the price that Louis Vuitton sold it in order to make ends meet. In fact, the exceptional (sometimes criticized) margins at Louis Vuitton did not arise from excessively high prices, but from the removal of all costs and damages due to intermediaries. Louis Vuitton’s competitiveness was therefore structural”

The Luxury Strategy

Other than the financial impact, own brand stores are crucial for perfect control over product placement and elevating the customers’ experience of the brand. See for example Dior’s landmark 12,000 sqm store at 30 Avenue Montaigne which integrates the historic home of Christian Dior with a museum, restaurant, a giant store and penthouse suite for the most exclusive of guests. The other important element is the human aspect. Well trained sales staff are crucial in story telling, explaining the quality of the products, and justifying the price. From Kapferer:

“Our anti-law number 12, ‘Luxury sets the price’, is applied to the letter here: the role of the store and the sales personnel is indeed to make the potential purchaser understand all the refinements of a product, all those aspects that make it a luxury product. This leads us to a conclusion that is surprising for classic marketing: the true role of the salesperson is not to sell the product – it is to sell the price.”

The Luxury Strategy

Just to reinforce the point on complete adherence to a 100% own-brand retail strategy, look at how Jean Jacques answered the question on whether they would consider doing duty-free/wholesale in Hainan:

And we'd love to do business in Hainan because there's significant business to be done there, but not at the expense of our business philosophy, which is to control the business we do in our own retail stores. So you will not see Vuitton or Dior wholesale stores just because we want to be in Hainan, no way. It will never happen.

Jean Jacques Guiony (CFO), Q3’22 earnings call

The below data from Morgan Stanley shows how important own-brand retail is for Louis Vuitton. The whole industry has been following suit, and the proportion of directly owned retail has been steadily on the rise.

Building brand equity

Positioning luxury brands - luxury is superlative, not comparative (Anti-Law #1)

At the heart of every traditional consumer product is a brand positioning matrix, which tries to articulate the unique value proposition or advantage that one brand has over another. Not so in luxury. According to Kapferer, “luxury is superlative, not comparative”. The beauty of luxury is that no one can definitively say whether a Louis Vuitton bag is better than an Hermes bag because that concept doesn’t even make sense. Each luxury brand is its own universe with its own identity, making them difficult to compare except in very vague terms. For example, Louis Vuitton’s brand identity can be tied to travel and a global lifestyle due to its origins as a producer of high-end leather luggage trunks. Hermes’ identity in premium leather goods is tied to its origins as a producer of high-end horse saddles. A consumer’s preference for one or the other or both is largely a matter of personal tastes. Consequently, that is why proximity of luxury stores next to each other on high-end streets is not a problem. In fact, they only strengthen each other from an image and social codes point of view.

Marketing and communication

In luxury, marketing and communication is essential in order to create the dream and to recharge the brand’s value, not in order to sell (Anti-Law #9). That is the key difference to normal products. Marketing in luxury is all about creating the impression of privilege and exclusivity - the feeling of “virtual scarcity” to complement the aforementioned physical scarcity around the product and distribution. This often takes place via multiple channels: 1) advertising (often not mass media like TV, but selective print and outdoor), 3) sponsorship of exclusive events 3) use of high-status brand ambassadors as influencers, and 4) the connections to art.

“The brand is a transmitter of taste: as such it should be a sign of ‘good taste’. In order to be recognized as such, it should display the visible signs of its adoption by those who make the front covers. It should be present in the high places of taste, living culture, and fashion, a little, as well. Luxury brands need to maintain an image that is classy, admirable, as well as instantly recognisable.”

The Luxury Strategy

Luxury brand marketing is often about trying to depict a certain universe or desire around a lifestyle, but never a promise. That is why most advertising depicts the products in a dreamlike way. The luxury brand is experiential first and foremost. Its language is mostly non-verbal: it is primarily visual and sensory. It is more its way of doing things, its refences, and aesthetics that are designed to weave the emotional relationship with its audiences.

While advertising is important, according to Kapferer it is not the essential vector of marketing for luxury. The essential vectors are events that are simultaneously exclusive and incomparable, intensely translating the brand’s values, and to which only a minority are invited (Anti-Law #8: Protect clients from non-clients). Sponsoring events rather than specific competitors is absolutely critical, since that way all aspects of the experience can be controlled. Louis Vuitton sponsors the Louis Vuitton Cup, a sailing event, not any specific boat. Hermès sponsors the Grand Prix de Diane, a horse race, not any specific horse. The events that are sponsored must be coherent with the universe of the brand’s core, its roots (Louis Vuitton and travel, therefore boats; Hermès and horses).

The role of brand ambassadors

The discussion here in the book is very interesting. We all know that luxury brands often use celebrities in their ad campaigns, which seems to contradict Anti-Law #16: Keep stars out of advertising. However, Kapferer goes on to explain an important nuance: there’s a difference between paying a big star to appear in an ad to try to elevate a non-luxury brand into luxury, and using important people as ambassadors who match up to the brand’s elite luxury status. In the latter case, you are placing yourself within the concept of ‘ordinary product for extraordinary people’, which draws status-conscious people to the brand. This is very much consistent with Anti-Law #6: The luxury brand dominates the client.

Louis Vuitton through the years has been quite thoughtful about using important people to associate with its products. Below is one of the more famous Louis Vuitton ads from early 2000s, showing Mikhail Gorbachev (former President of the Soviet Union) in his car in front of the Berlin Wall, using the signature brown monogram Louis Vuitton bag. Below that is a more recent ad in the lead up to the 2022 World Cup with football legends Lionel Messi and Cristiano Ronaldo casually playing chess on a Louis Vuitton trunk, a hark back to the brand’s roots in creating high-end travel trunks (which are also used to transport the World Cup trophy).

Quoting Kapferer, “the star’s status should never be higher than the brand”. Louis Vuitton has had a host of famous stars as its brand ambassadors over the years, including Madonna, Jennifer Lopez, Kate Moss, Scarlett Johansson, and Angelina Jolie. These are all people who’s stature lives up to the brand’s recognition, and in the carefully crafted images of these campaigns the star never outshines the products. Looking at the other brands, Dior’s famous Lady Dior bag has an iconic association with Princess Diana. The bag was originally created in 1995 in honor of the royal, with its design having touches of Dior’s history (Dior charms reminiscent of the lucky talismans that its founder Christian Dior was famous for carrying) as well as incorporating modern sophisticated touches which Diana was known for. The bag is estimated to account for over 50% of Dior bags' sales today. Not just Louis Vuitton and Dior however, LVMH’s alcohol brands employ the same playbook through thoughtful and public association with powerful personalities and prestigious events. Don Perignon’s campaign with actor Cristoph Waltz and Lady Gaga, Moet and Chandon with Scarlett Johansson and Roger Federer, and Moet’s prominent display in Leonardo DiCaprio’s The Great Gatsby where his character and guests drink it by the bottle, are all good examples of the use of powerful brand ambassadors.

The “artification” of luxury

Anti-Law #17: Cultivate closeness to the arts. The luxury brand is a promoter of taste, like art. It maintains close links with art. But luxury is not a follower: it is creative, it is bold.

The Luxury Strategy

Luxury brands use art in both a direct manner (creativity in product design), as well as in an indirect manner, linking art to the brands’ name and image - to quote Kapferer “as a promoter of good taste”. These strategies are generally extremely costly and can only be implemented in a systematic manner by the largest brands, hence creating some barriers to entry. Many of the luxury brands have their own foundations which sponsor art exhibitions, such as the Monet exhibition by the Louis Vuitton foundation currently running in Paris. Secondly, luxury brands often run exhibitions/museums showcasing their own artists or the brand’s history, such as Louis Vuitton’s “200 Trunks, 200 Visionaries” (below) which had a global tour. Dior in particular stands out here, depicting their founder Christian Dior as not simply a designer but an artist of the highest calibre (he was in fact an art gallerist before creating the fashion house).

Finally, brands often collaborate with artists to create limited edition ranges. For example, Dior frequently invites artists from different backgrounds to revisit its iconic Lady Dior bag. Everyone from poets to architects, painters and photographers have drawn on their creative worlds to create a new version of the classic handbag. The price of these is typically much higher than normal.

Heritage vs. Innovation

While LVMH itself is a relatively young company (having been established in 1987), the brands that it acquires are anything but. There is a real “Lindyness” to the portfolio, with many of the brands over 100 years old and having stood the test of time:

Louis Vuitton was founded in 1854

Moet & Chandon was founded in 1743

Dior was founded in 1946

Fendi was founded in 1925, acquired in 2001

Guerlain was founded in 1828, acquired in 1994

Tiffany was founded in 1837, acquired in 2020

Loewe was founded in 1846, acquired in 1996

Moynat was founded in 1849, acquired in 2010

Tag Heuer was founded in 1860, acquired in 1999

Berluti was founded in 1895, acquired in 1993

Rimowa was founded in 1898, acquired in 2016

Loro Piana was founded in 1924, acquired in 2013

This element of timelessness and heritage is important as it gives the brand identity and a sense of permanence.

“Identity is not something that can be bolted on: it is nurtured from the brand’s roots, its heritage, everything that gives it its unique authority and legitimacy in a specific territory of values and benefits. It translates its DNA, the genes of the brand.”

The Luxury Strategy

However, there is a conceptual mistake often made that luxury needs to stay consistent with its heritage and tradition. That is wrong, as static brands become boring, and ultimately lose touch with the tastes and ideas of their times. It’s a fine balance. On the one hand, every brand has a DNA to which it needs to stay consistent, otherwise it loses its soul. This includes iconic products, references to key shapes, colours or imagery, and a set of core values. At the same the products need to be updated with contemporary designs, technology, materials, new values (e.g. sustainability) and modern brand ambassadors. The most successful brands over the past decade have been those that have successfully mixed heritage with innovation - Louis Vuitton, Hermes, Dior, Chanel, as well the large brands owned by Kering - Gucci, Bottega, and Balenciaga.

Louis Vuitton’s iconic monogram bags have a storied history, linking back to the brand’s origins in 1856 when it was producer of a high-end luxury luggage trunks. And while the monogram is timeless both in style and durability, Louis Vuitton has had to create new lines to keep its image fresh, relevant and exclusive. A notable example is its 2013 launch of the Capucines handbag, which played a major role in revitalising the brand from a period of stagnation.

For about two decades during the 1990s and 2000s Louis Vuitton’s monogram bags were selling extremely well, with its at the time CEO Yves Carcelle saying the brand required little innovation due to the high demand. However, he overplayed his hand and during 2010-2014 the brand’s organic growth started lagging the industry, particularly as the early Chinese adopters were now looking for more exclusive, expensive brands. Louis Vuitton was quick to realize that it had a problem and had to go through a reinvention, which required not only a leadership change (new CEO Michael Burke appointed in 2013), but also change in creative direction with the appointment of new Creative Director Nicolas Guesquiere (ex-Balenciaga) in that same year.

Under Nicolas’ oversight, the Capucines was designed and launched in 2013 as part of a strategy to shift the product mix away from its monogram canvas to leather handbags. The bag paid homage to the history of the brand (being named after the street of Louis Vuitton’s first Paris store in 1984), but it was a modern, sophisticated bag, using the same premium full-grain calf leather used in Hermes bags, and retailing for a significantly higher price than any of Louis Vuitton’s canvas bags (€3,500 vs. average price of €600 for canvas bags at the time). Using all the physical and virtual scarcity strategies discussed earlier, the Capucines turned into a complete breakthrough for the company, being instantly sold out all across Europe, and in turn rejuvenating Louis Vuitton’s image particularly in the high-end leather bags segment. The design of the bag was also a perfect canvas for new variations - Louis Vuitton has introduced new annual Arty Capucines limited edition ranges in collaboration with various artists.

What we see above with Louis Vuitton’s Capucines and earlier with Dior’s Lady Dior bag is that limited editions and collaborations is a frequently used strategy to keep the brand fresh. Sometimes this means collaborations not just with individual artists and creators, but other brands, like Louis Vuitton’s capsule collection with street fashion brand Supreme. As shown below, the collection combined the LV monogram with the Supreme logo on sneakers, baseball shirts, and jackets, as well as traditional duffles and backpacks. Streetwear has become more relevant for younger consumers, and collabs like this have become an effective way for luxury brands to recruit a new generation. Similarly Dior dropped a collaboration with Nike’s Air Jordan. These limited edition shoes priced at $2,200 sold out in minutes, and was the most successful luxury collaboration of 2020.

Other times it could mean limited edition ranges linked to current events. In May 2018 for the British royal wedding of Harry and Meghan, Louis Vuitton released a limited edition collection of bags with the Union Jack. Only 85 were available and only in its flagship London store. While all these limited edition capsules generally account for a very small part of a luxury brands’ total sales (<1%), they create enormous publicity, keep the perception of brand fresh, and introduce new customers.

Brand equity and financial performance

So how successful has Louis Vuitton been in building brand equity? For this we can turn to the various industry surveys that measure the most valuable brands in the world. For example Kantar BrandZ recently ranked it #10 most valuable across all global consumer brands.

Amongst just luxury brands, Louis Vuitton has consistently ranked at the top in surveys by BrandZ and Interbrand, and this has been the the case for over a decade now. Dior has been rapidly on the rise as well.

Ultimately the desired outcome of high brand equity is to create the perception that the value of the product is higher than the actual price consumers are paying (Anti-Law #11). This allows for significant pricing power, and according to analysis from Bernstein, pricing power is the most important determinant of luxury company profitability - “The implication for luxury brands is the futility of dropping cost cutting to the bottom line, because the only thing that affects your profitability in the long term is price elasticity, meaning that percentage profitability is really driven by emotional connections”.

Similarly, Kapferer warns against the temptation of cost-cutting. Managing luxury brands requires significant investment in product design and materials, brand marketing, store ownership and operations, hiring of creative talent, staff training, amongst other things. All of these elements are essential for growing brand equity, and thus cost cutting, while raising near term profits, may impact the long term value of the brand. Of course, these high capital requirements is a key reason for why large brands with the most scale have the advantage, and why the likes of Louis Vuitton, Dior, Hermes and Gucci have been growing faster than the overall luxury market over the last few years.

Finally, the success of Louis Vuitton can be seen in the below comparative analysis from Morgan Stanley. Louis Vuitton’s brand equity translated into clear leadership in terms of revenue scale and profitability.

The playbook applied to other brands

To be fair, the success of Louis Vuitton and Dior has not been replicated everywhere across LVMH’s portfolio. Some of its fashion brands like Celine and Marc Jacobs have been nowhere near as successful over the last decade, with their respective relaunch attempts experiencing mixed receptions. Ultimately creativity and innovation are just as important as the commercial aspects of luxury brand management, and these are difficult to formulate as they depend on the genius of the creator. Jewelry brand Bulgari however has been a notable success. Since being acquired in 2011, LVMH has more than doubled Bulgari’s revenue and increased its profit by 5x, largely by following the same luxury playbook as described through this article - removing wholesale and focusing more on the retail experience, decreasing the range of inventory, investing in marketing and raising the brand image.

The big test will now come with its most recent acquisition of Tiffany & Co. As can be seen above, the jewelry brand’s performance has been relatively stagnant over the last decade compared to the other two branded jewelry peers. If LVMH can replicate its Bulgari success with Tiffany, jewelry can become another major pillar for its business.

To do this, the company has wasted no time in appointing a heavyweight team of LVMH executives to Tiffany, including Michael Burke as Chairman (he is CEO and Chairman of Louis Vuitton), Anthony Ledru as CEO (ex-EVP of Commercial at Louis Vuitton), and perhaps most prominently, Bernard’s 30 year old son Alexandre Arnault as head of Product and Communication (he was previously CEO of Rimowa at LVMH). Often considered as the more entrepreneurial of Bernard’s children, Alexandre is now responsible for the marketing efforts at Tiffany. And he started this stint with some big moves. In an attempt to revitalise and modernise the brand, in July 2021 Tiffany launched a provocative guerilla-style campaign with the slogan "Not your mother's Tiffany". Posters carelessly plastered all around New York and Los Angeles featuring denim clad models wearing the edgiest Tiffany pieces marked the brand's new beginnings under LVMH. It represented a rupture with Tiffany's past image and heritage and a nod to modernity. The response on social media has been divisive —some noted the campaign "disses" existing customers, while others deemed it a necessary move to attract the attention of Gen Z consumers.

While this campaign seemed very out of character with LVMH’s luxury playbook, it does highlight how sometimes a “Big Bang” rather than incremental approach is needed to revitalise a stagnant brand. Others such as Gucci and Balenciaga (owned by Kering) have implemented similar Big Bang relaunches often under new leadership in the past with great success. According to Alexandre Arnault, Tiffany’s silver sales saw their fastest growth in 5 years in the month of that campaign. Other initiatives to transform Tiffany are much closer to the traditional playbook. LVMH brought in Louis Vuitton’s go-to architect Peter Marino to completely redesign their New York flagship store to LVMH’s standards - this is due to reopen post its renovation in 2023. They have also launched a new concept store in Paris, increased prices across its core ranges, introduced new innovative products, and refocused on the ultra-wealthy clientele through exclusive special events. LVMH accepts that turning around Tiffany will be a long term effort, and time will tell whether this will be another success for the group.

Concluding Thoughts

The management of luxury brands is unlike that of normal consumer products, and the playbook revolves around 1) tight control of the entire supply chain from material sourcing to retailing, 2) premium pricing which can only increase over time 3) marketing that elevates the desire and dream-aspects of the brand, and 4) balancing heritage and creativity/innovation. LVMH has pioneered and continues to successfully execute many aspects of luxury brand management that are described in The Luxury Strategy. Their keen understanding of how to build brand equity for the long term together with sound capital allocation has led to superior returns on invested capital and share price performance.

One of the key takeaways for me from this luxury deep dive however is that while following the rules of luxury brand management is critical to avoid trivialization, and some structural advantages for the mega-brands exist, you cannot win by standing still. The key commercial elements described throughout this article need to be driven by astute executives, but also paired with the genius of a small number of talented creatives and designers. Ultimately luxury is as much about artistry and good taste as it is about managing inventory, pricing and distribution. Both of these groups need to have an uncanny ability to read market opportunities and gyrations, understand the cultural zeitgest, and respond both commercially and creatively in an appropriate manner. That is why managing luxury brands is no easy task - many brands including Louis Vuitton have stumbled along the way and have had to relaunch under new leadership. For any luxury business investor, the key risks to monitor are a loss of brand equity and cachet, stagnation in creativity/innovation, and managerial actions in managing the brand, which will ultimately translate to financial performance.

Good materials for further research into LVMH:

The Luxury Strategy: Break The Rules of Marketing To Build Luxury Brands Jean-Noël Kapferer

Interview with Bernard Arnault at Oxford University

Interview with Alexandre Arnault at Oxford University

LVMH: The Civil Savage (The Generalist)

How Louis Vuitton took over Asia (Asianometry YouTube channel)

This article is just impressive, great work! I love how you showed the translation of principles into business decisions.

Loved this, thank you so much!